Every year, the “Ecommerce Italia” report by Casaleggio Associati provides one of the most authoritative snapshots of the state of digital commerce in our country. The 2026 edition, presented in recent days, offers a particularly clear interpretation of the market’s current phase: less uncontrolled expansion, more selection and competition.

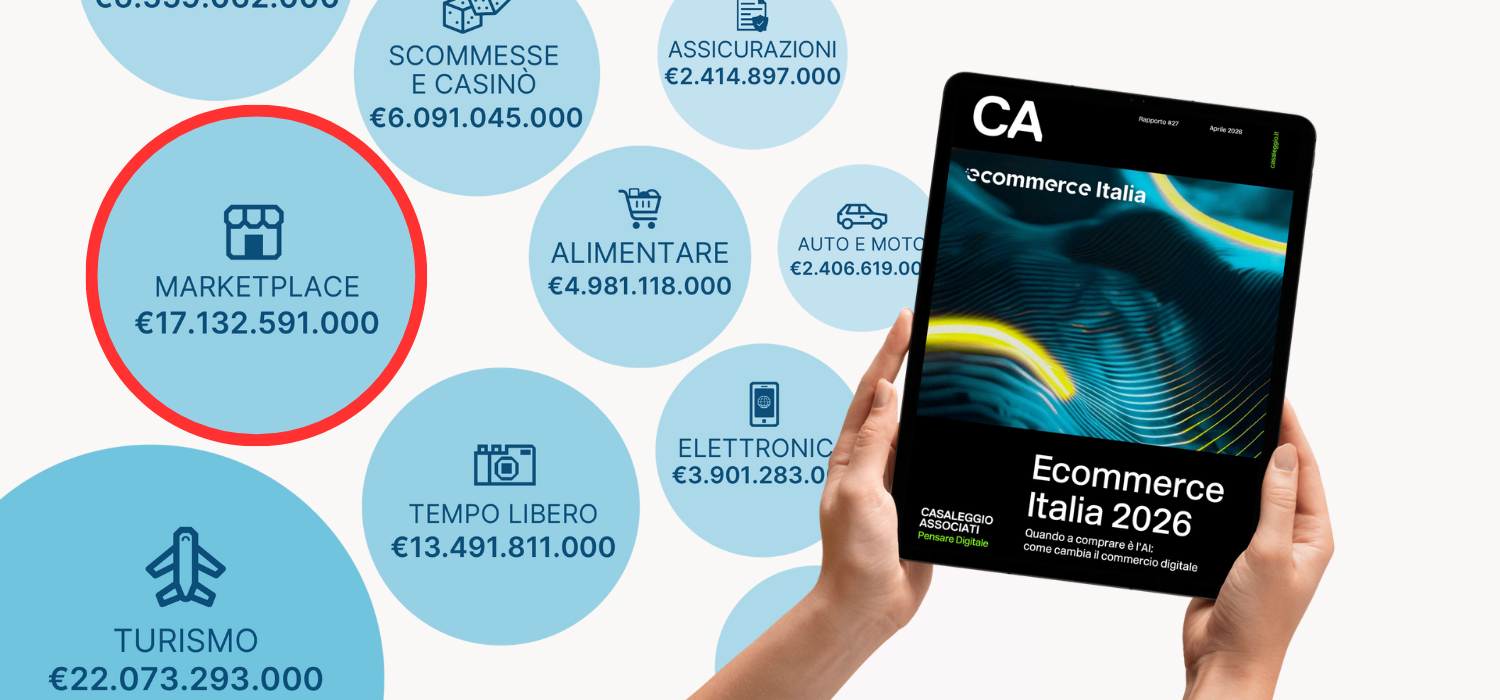

The total value of Italian eCommerce reached €90.6 billion in 2025, with a +6% year-on-year growth. A positive figure, but one that marks a slowdown compared to previous years and, above all, signals the entry into a new phase of maturity.

Beyond the numbers, among the most interesting dynamics emerging from the report, one in particular stands out for its impact and implications: the growth of marketplaces and their role in redefining the operational standards of eCommerce, especially in logistics.

In this article, we want to analyze this very phenomenon, because today, more than ever, it is not price or product that makes the difference, but delivery.

The rise of marketplaces: from channel to dominant infrastructure

If we look at the numbers, the signal is unmistakable. In 2025, the marketplace segment grew by 15.7%, more than double the market average. But the quantitative data alone is not enough to explain the scale of the phenomenon.

What is changing is the very role of marketplaces. They are no longer simply platforms that intermediate between supply and demand; they are gradually becoming central infrastructures of digital commerce, capable of integrating catalog, payment, customer relationships, and, above all, logistics.

This shift is also reflected in rankings: top positions are consistently occupied by large global platforms, while smaller operators struggle to maintain visibility and frequency of interaction with users.

Their strength lies not only in the variety of their offerings or price competitiveness, but in their ability to build a consistent, predictable, and replicable experience. In other words, a standard capable of generating the most significant impact on the market.

When the standard changes, delivery changes too

For years, delivery was considered an ancillary component of the shopping experience. Important, of course, but secondary to product, price, or brand. Today, this hierarchy has been reversed.

Marketplace platforms have progressively shifted attention to the entire purchasing cycle, transforming logistics into a central element of the value proposition. It is no longer about “shipping an order,” but about ensuring a smooth, predictable, frictionless experience.

As a result, certain features—fast delivery, accurate tracking, easy returns management—are no longer perceived as competitive advantages, but as basic requirements.

This is the so-called “Amazon effect”: a standard that emerges in a specific context and then extends, almost automatically, across the entire market. Users no longer distinguish between those who can afford advanced logistics infrastructure and those who cannot—they expect the same experience everywhere. This creates growing tension. On one hand, operators are required to adapt; on the other, the cost of doing so is far from negligible.

The structural limits of the traditional model

This is where the critical issue emerges. The home delivery model, on which much of eCommerce has been built in recent years, now shows clear limitations.

It is not only a matter of costs, although these remain a determining factor. Last-mile delivery is, by definition, one of the most complex and expensive stages of the logistics chain. But the problem is also structural.

Door-to-door distribution, especially in fragmented urban contexts, involves inefficiencies that are difficult to eliminate: failed delivery attempts, low shipment density, and not always predictable timing. All elements that impact both margins and the perceived quality of the customer experience.

With increasing volumes and the growth of recurring purchases—another dynamic highlighted in the Casaleggio report, which emphasizes how eCommerce is increasingly tied to the frequency of interaction with users—these issues become even more evident. The result is a system under pressure, struggling to sustain the standards imposed by the marketplace model.

Towards distributed logistics: the growing role of Out Of Home

In this scenario, a different approach to delivery is emerging, based on a proximity logic. Out Of Home solutions (Pick-up Points and Lockers) are no longer perceived as an alternative, but as a concrete response to the limitations of the traditional model.

Their advantage is twofold. On one hand, they offer greater flexibility to consumers, who can choose when and where to collect their orders, freeing themselves from the constraints of home delivery. On the other, they allow logistics operators to optimize flows, reduce costs, and increase efficiency. It is no coincidence that this model is spreading precisely in more mature contexts, where pressure on margins and operational performance is higher.

In Europe, and increasingly in Italy, logistics infrastructures capable of covering territories extensively are emerging. Among these, companies like GEL Proximity represent a clear example: a network of over 500,000 pick-up points and lockers that brings delivery closer to the end consumer while reducing last-mile complexity.

Learn more about GEL Proximity solutions for eCommerce delivery and returns.

From logistics as a cost to logistics as a competitive lever

Perhaps the most significant change is this: logistics is no longer just a cost center to optimize, but a strategic lever capable of directly impacting business performance.

An effective delivery experience not only improves customer satisfaction but also influences key metrics such as conversion rate, average order value, and customer retention.

In an increasingly competitive market, where products are easily comparable and prices quickly aligned, these elements are what truly make the difference.

Integrating flexible delivery solutions, such as pick-up points or lockers, does not simply mean expanding available options—it means responding to a structural shift in user expectations.

The real game is played after checkout

The Ecommerce Italia 2026 report describes a market that continues to grow, but in a more selective and conscious way. In this context, marketplaces are exerting an influence that goes far beyond market share. They are defining the rules of the game.

And among these rules, logistics is taking on an increasingly central role. No longer the final stage of the purchasing process, but a determining element of the overall experience.

For eCommerce businesses, this means that the challenge is no longer just selling better, but delivering better—more efficiently, more flexibly, and closer to the real needs of consumers. Because in the new balance of digital commerce, that is exactly where the most important game is played: after checkout.